Buy now, pay later won the 2020 holiday season. Why? People were able to stretch their funds with this useful payment option.

In our opinion, this useful feature at checkout is not going anywhere.

What is buy now, pay later?

Buy now, pay later, otherwise known as BNPL, is a purchase you can receive immediately and then pay for in equal installments.

BNPL has been around for years but became very popular throughout the pandemic. More people started shopping online and had less money to spend upfront.

Now, most retailers have a specific company they use for BNPL. So, you might see Afterpay, Klarna, or Affirm at checkout.

BNPL is a kind of installment loan that divides your purchase into many equal payments. The first one is due when you checkout. Following payments are billed on your card until you have fully paid off the purchase.

What is an example of buy now, pay later?

A lot of companies split the purchase into four payments. This divides your purchase into four equal parts. Each payment is due two weeks apart, with the first one being due at checkout.

An example of this is if you buy something for $300. First, you pay $75 at checkout. Now you have three payments of $75 remaining. Each is due two weeks apart. If you pay all your payments on time, your purchase will be paid off in six weeks.

This 4-payment-arrangement doesn’t typically charge interest, but some BNPL plans charge APRs as high as 30%. Late fees can be around $10 and generally are no greater than 25% of the order.

Why is buy now, pay later so popular this year?

There are a lot of factors against the consumer this year. Discounts will be harder to find. Supply chain problems are hiking prices through the roof. And a lot of people are still recovering financially from COVID-19.

However, Deloitte expects a 7% to 9% increase in holiday spending compared to 2020.

Lots of people are looking for the best way to stretch their cash. We all want to spend money on the people we love and get them the gifts they deserve. BNPL can help you do that.

Is buy now, pay later the new way to shop?

Minimum wages are not going up, and inflation is on the rise. Furthermore, online shopping is the primary method of shopping for younger people.

Millennials and Gen Z are the most likely populations to use BNPL. And these generations make up a large portion of the current and future workforce. They also have a lot of spending power.

Stores that don’t embrace this payment method shortly run the risk of falling behind and losing out on an entire market of shoppers.

What are some things to consider about buy now, pay later?

Many economists only recommend BNPL plans for essential expenses because it is still a form of debt.

You should also find a plan with little or no interest.

Buy now, pay later is a good idea for the holidays if you keep track of how much you are buying and what your monthly payments will be. You do not want to go into more debt than you can afford.

What are the Pros and Cons of Buy Now, Pay Later?

There are many pros and cons to BNPL.

BNPL pros

- Plans available with zero interest

- No required minimum credit score

- Offered by most significant retailers online

BNPL cons

- Some plans include interest

- Some plans include late fees

- Payments might not be sent to credit bureaus, so you may not build credit

- It’s easy to spend more than you have

What are some alternatives to buy now, pay later?

It might be wiser to pay with a credit card for some people.

With most credit cards, you get cashback and rewards and report payments that you make on time to the credit bureaus.

Having a history of payments being made on time builds your credit score and helps you get better financing moving forward.

What are some websites that let you buy now, pay later?

- Affirm works with retailers like Pottery Barn, Adidas, and Walmart. Its interest rate depends on the retailer. Some stores charge no interest, while others charge as high as 30% APR for a year. They never charge fees for late payments.

- Klarna is used in Macy’s, Foot Locker, and Sephora stores. It has a Pay in 4 model that does not charge interest. However, if they cannot collect payment after two tries, it sets the fee up to $7.

- Zip used to be called Quadpay. It can be used wherever Visa is accepted after downloading the Zip app. Zip charges a $1 fee for each payment you make and either a $5, $7, or $10 late fee depending on where you live.

- PayPal has Pay in 4 payment plans online and via their app at Bed Bath & Beyond, Target, and Best Buy stores. There are no late fees or interest.

How does buy now pay later compare to layaway programs?

Layaway programs are when you pay a little bit at a time until you pay off an item in full, at which point you take it home.

Buy now, pay later is like layaway in reverse. You get your item right away and then pay it off over time.

Can buy now, pay later impact your credit score?

When you apply for a buy now, pay later program, they often run a soft credit check before approving you. This does not affect your credit score.

However, while credit bureaus do not track some BNPL plans, others are. This means that if you miss a payment, it can negatively impact your score.

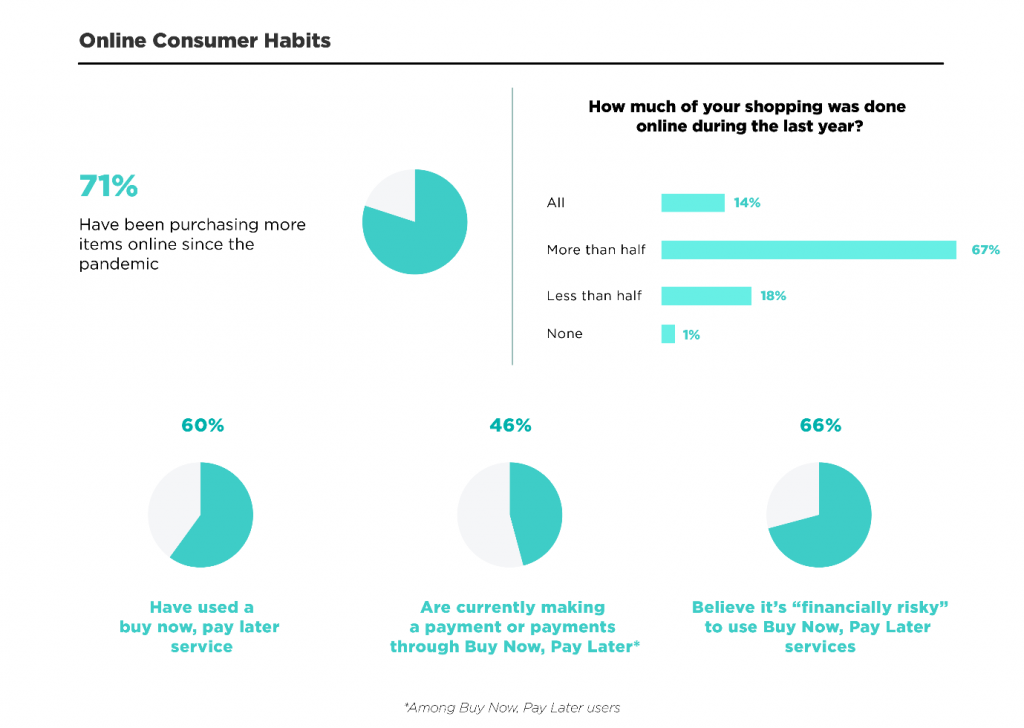

Almost 40% of consumers missed at least one payment of their buy now, pay later installments. Around 75% of those people had a hit on their credit score.

Do people spend more when they buy now, pay later?

What entices businesses to offer these services, even though they pay BNPL companies fees?

These programs encourage people to spend more in the long run because they think about the short term. If you only have $100 to spend, you can buy four $100 gifts for $25 each using BNPL. But in the long run, you are spending $400.

In addition, you may have to spend late fees or high-interest rates. It might also be hard to keep track of all the deadlines for payment if you used BNPL for multiple purchases.

If you put the buy now and pay later payments on your credit card, you may end up with the debt you initially dodged.

If you can afford the item in the long run but don’t have all the cash upfront, BNPL is a great option and can let you buy the gifts you want to get your loved ones. But if you do not think through your buy now, pay later purchases, you can end up with a massive headache.

What are some buy now, pay later statistics?

Here are some facts about buy now, pay later.

- Klarna has over 90 million people using their service, with nearly 2 million purchases made every day.

- Cardify states that out of 2,000 verified buy now, pay later shoppers, 45% said they were planning to pay for some of their gifts using BNPL.

- From this study, 65.7% said they would use debit cards, while 54.6% used credit cards.

- 8.6% of respondents were willing to pay for all their gifts using buy now, pay later.

- A Debt Hammer study discovered that 58% of people expect to get a payday loan for a holiday, compared to 66% who opt for BNPL.

Final thoughts

Buy now, pay later took over the holidays and is the new way to shop.

With the power of Millennials and Gen Z, this payment method has grown in popularity and will continue to do so. Many of this population can only afford things when they use this method because of low wages and high prices.

Stores that do not keep up with the trends, and companies that do not continuously improve their BNPL options, will miss out on a vast market.

Buy now, pay later is the latest shopping trend and will continue to be so.

{kind=link}